Harvesting and Merchandising Highlights

- Forests of the U.S. Southeast are large and growing, and only a small percentage is harvested each year

- When harvested, the products from each tract are merchandised into multiple markets, from high-value timber like dimensional lumber and other building products, to low-value pulp and bioenergy materials, where bioenergy typically provides the lowest revenue per ton. We believe that our purchase of that fiber is an integral part of growing more trees and improving forest health

- For 2H 2021, which corresponds to the current Track & Trace® data set reporting period on our website, Enviva’s merchandising percentage was on average 35% across our procurement areas; for 59% of harvested acres, our merchandising percentage was less than or equal to 30%

- 12.4% of our final harvest acres in 2H 2021 came from forest tracts where our merchandising percentage was greater than 70%. Reasons for this include hurricane damage, multi-stage harvesting, and ecological or economic reasons that a harvest was predominantly pulpwood

- Healthy markets lead to healthy forests which continue to grow, especially when the forest community is committed to ensuring forests remain forests – a commitment Enviva obtains from all its fiber suppliers

In the U.S. Southeast there are more than 380 million acres of forestland and 10 billion tons of wood.1 According to U.S. Forest Service FIA data2, only approximately 3% of the timber lands in the states where Enviva sources wood is harvested each year. U.S. Southeast working forests are predominantly privately owned. Many of these forests are grown for timber production and, after harvesting, they are replanted or naturally regenerated as part of the forest regeneration practice that has been ongoing for centuries in the region. “Clear cutting” and “thinning” are common and preferred methods by which tracts in the working forest landscape of the U.S. Southeast are harvested.3

Markets for forest products impact landowner decisions about how to utilize their land and are a key reason landowners continue to invest in forests by planting seedlings, cultivating natural regrowth, managing these timberlands, harvesting, and consistently repeating the cycle. As a result of landowner decisions and care for their forests, for every ton of wood harvested from the working forests of the U.S. Southeast, approximately 1.75 tons grow each year.4

-

Markets Determine Value

The process of harvesting timber from healthy stands serves multiple markets, including saw timber, pulp, and biomass, and supports a range of forest-related products, including utility poles, dimensional lumber, paper products, packaging materials, and bioenergy products. Loggers methodically “merchandise” each product class on the harvest site in order to deliver each class to the highest-paying buyer.

For example, when manufacturing furniture and building products, the sawmilling equipment of the buyers of these top-dollar commodities require a minimum length and width of the raw material. This means their purchases are of the tallest, straightest, and larger diameter parts of the harvest, which are typically the stem of the tree. Enviva augments the productivity of these working forests by purchasing the parts of the harvested wood that are generally not utilized in other higher-value markets, such as the tops and limbs of trees, crooked or diseased trees, slash, understory, and thin tree lengths. The high-value markets are typically defined as those markets that manufacture products with permanent or semi-permanent carbon storage, such as telephone or utility poles, furniture, manufactured building materials, and dimensional lumber, whereas low-value markets are typically paper, pulp, and bioenergy markets. Naturally, loggers and landowners seek to efficiently merchandise harvests to the highest-value markets, rather than to purchasers like Enviva, which generally provide the lowest revenue per ton to the supplier.

Enviva’s sourcing also includes tracts located in regions where, due to land and soil conditions, it is difficult to grow sawtimber, or where there are insufficient lumber markets. In these areas, landowners often harvest and regrow for the pulpwood markets. Regardless of the type of tract from which Enviva sources, Enviva does not accept wood from harvested land when the landowner does not intend to keep the land as forest. This is a condition of Enviva’s fiber purchase agreements.

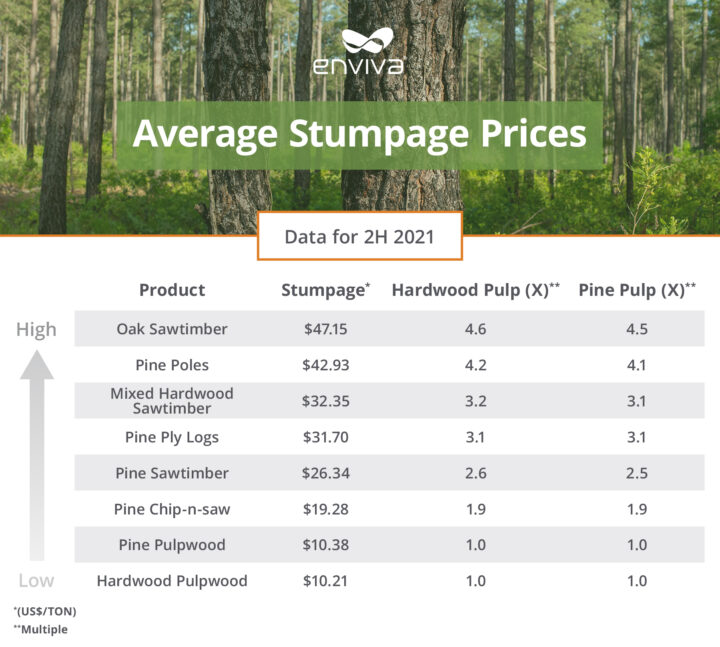

The chart below depicts data provided by TimberMart-South for wood purchases across the U.S. Southeast from July to December 2021 (corresponding to the current Track & Trace data set reporting period on our website).5 As noted, “Stumpage” (which is the price landowners receive when selling their harvested timber) for high-value commodities like sawtimber and utility poles is much higher than for pulpwood. In fact, as the chart illustrates, tons that can be used in high-value Oak Sawtimber production, for instance, were purchased on a stumpage basis at 4.6 times the cost of the tons that did not meet the length, width, or quality specifications of those markets, like Hardwood Pulpwood. Our procured stumpage, which includes even lower-grade products than pulpwood, like slash and understory, is purchased at an even lower per-ton cost. This means that landowners and loggers have a clear financial incentive to carefully merchandise the various products from a harvest to maximize deliveries to the highest-paying customers and minimize deliveries to low-value residuals purchasers like Enviva.

South-wide stumpage data provided by TimberMart-South

-

Enviva’s Track & Trace® (T&T®) Merchandising Data

Since its inception, a key goal of the Track & Trace program has been to provide leading transparency surrounding Enviva’s sourcing practices while maintaining supplier privacy within the limits of accessible data. T&T data aggregation has continued to evolve and becomes more robust each year.

Reported T&T data includes only Enviva’s primary sourcing, which means wood procured directly from working forests. Reported T&T data does not include wood procured from secondary sources such as sawmills and other forest products industry constituents.

Prior to any harvest from which Enviva is considering procuring wood, Enviva, suppliers, and landowners estimate the percentage of the tracts’ total volume that is expected to be harvested and allocated to Enviva from the proposed harvest (our “merchandising percentage”) and, by implication, the percentage that is likely to be purchased by buyers of higher-value commodities.6

Here’s how it works: Tracts in our data set are reported based on the total acreage that is intended to be harvested by a landowner at the time the tract is evaluated and pre-approved, in accordance with our Responsible Sourcing Policy. For each tract, we record our merchandising percentage. We report this merchandising percentage only on the final harvests (clear cuts and seed tree cuts) and arboriculture/salvage cuts. It is important to note that, at times, landowners will undertake multiple-stage final harvests for a range of reasons, including harvests for specific species (e.g., oak hardwood), harvests that require different equipment at various stages, and high-grading. As a result, our estimated merchandising percentages for certain tracts may overstate the relative percentage taken by Enviva as they do not account for volume taken by other buyers in the previous stages of the final harvests. Additionally, we expect our merchandising percentage to vary somewhat from data period to data period based on landowner harvesting decisions and individual characteristics of harvested tracts.

-

How We Characterize Our Sourcing

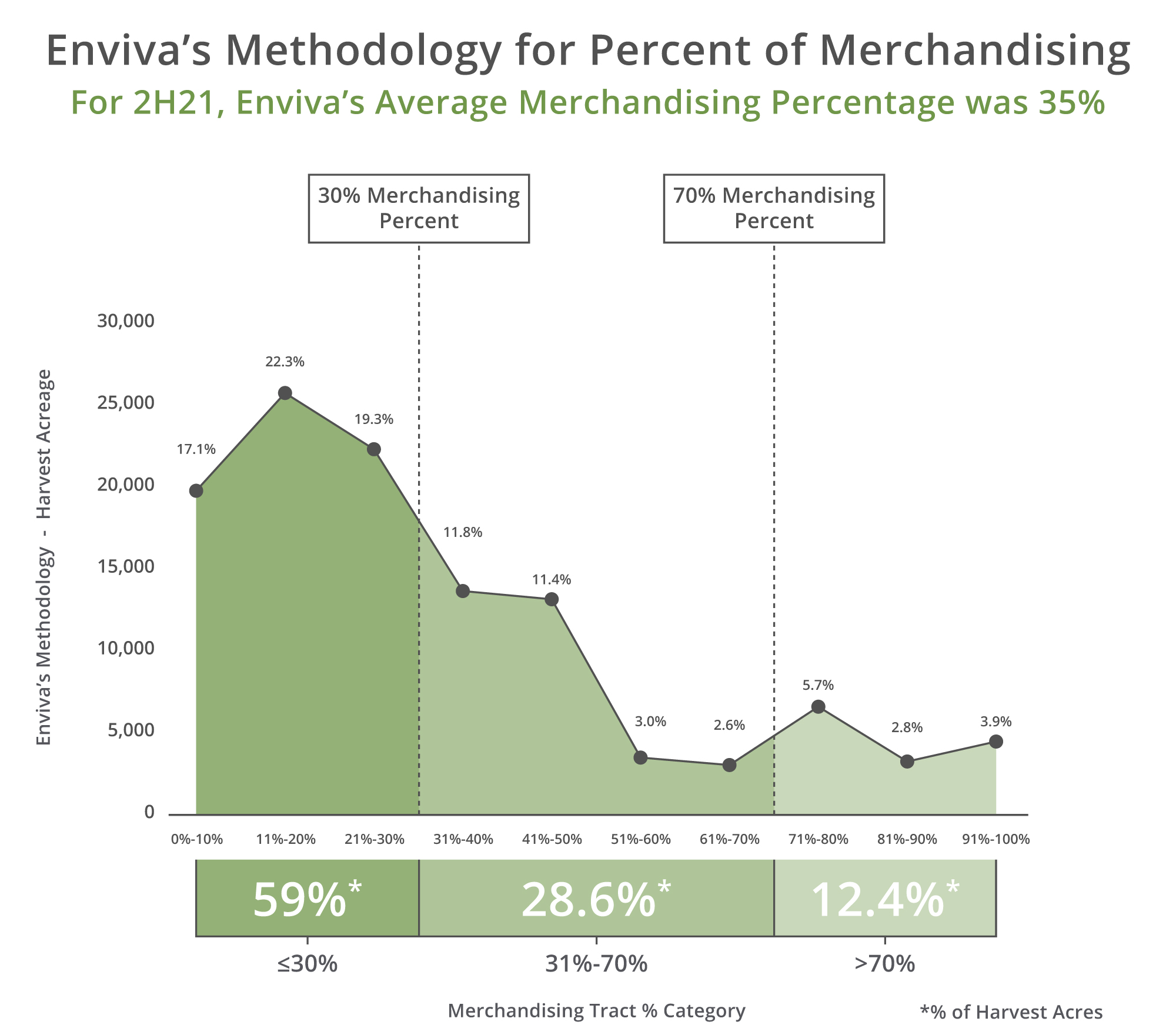

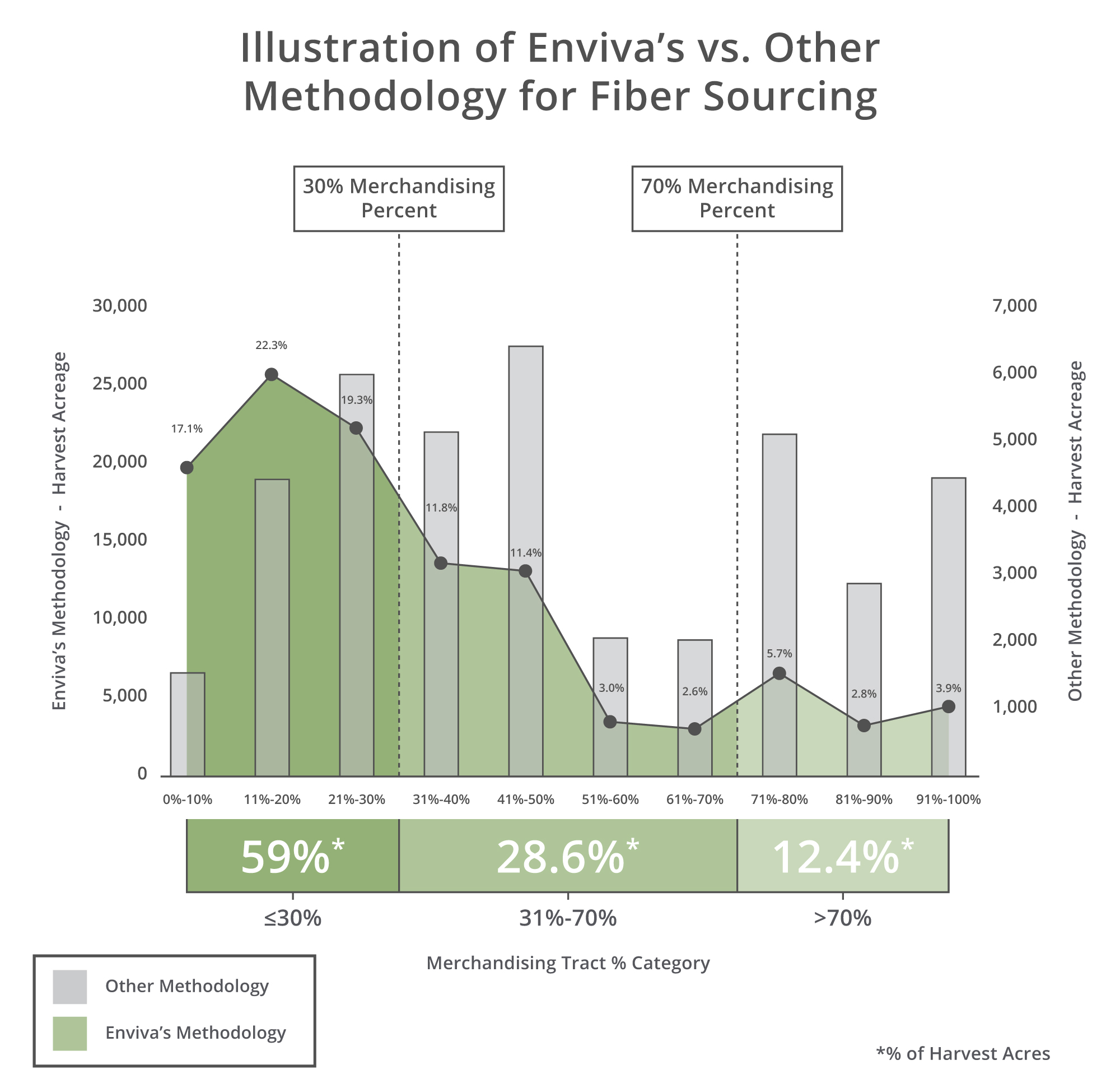

The chart below categorizes the total number of harvest acres by merchandising percentage for the second half of 2021. For instance, if we expect to procure 32% of the material from a 100-acre harvest, the data set below will include 100 acres categorized as “31% – 40%” merchandising percentage because, as noted above, harvesting practices generally produce a stream of multiple products across all acres and trees on the land.

This data includes neither secondary material (e.g., sawdust, shavings, and other byproducts from other forest products industries), as noted above, nor wood sourced from thinning activity. As detailed in our T&T data set, secondary material accounted for ~20% of our volume and thinnings accounted for an additional ~18% of Enviva’s volume in the second half of 2021.

Based on the methodology outlined above, the chart below illustrates that, for the period from July 1 to December 31, 2021, our average merchandising percentage was 35%, with 59% of the acres falling within a merchandising percentage of 0 to 30%. 12.4% of the acres fall within a merchandising percentage greater than 70%. Given the pricing differential outlined between high-value and low-value products generated from a harvest, it is unlikely that a landowner would choose to harvest a tract solely on the basis of low-value, low-percentage allocations to companies like Enviva, which generally provide the lowest revenue per ton to the landowner.

For those unfamiliar with the forest industry and harvesting, we understand this data can be confusing and potentially misunderstood.

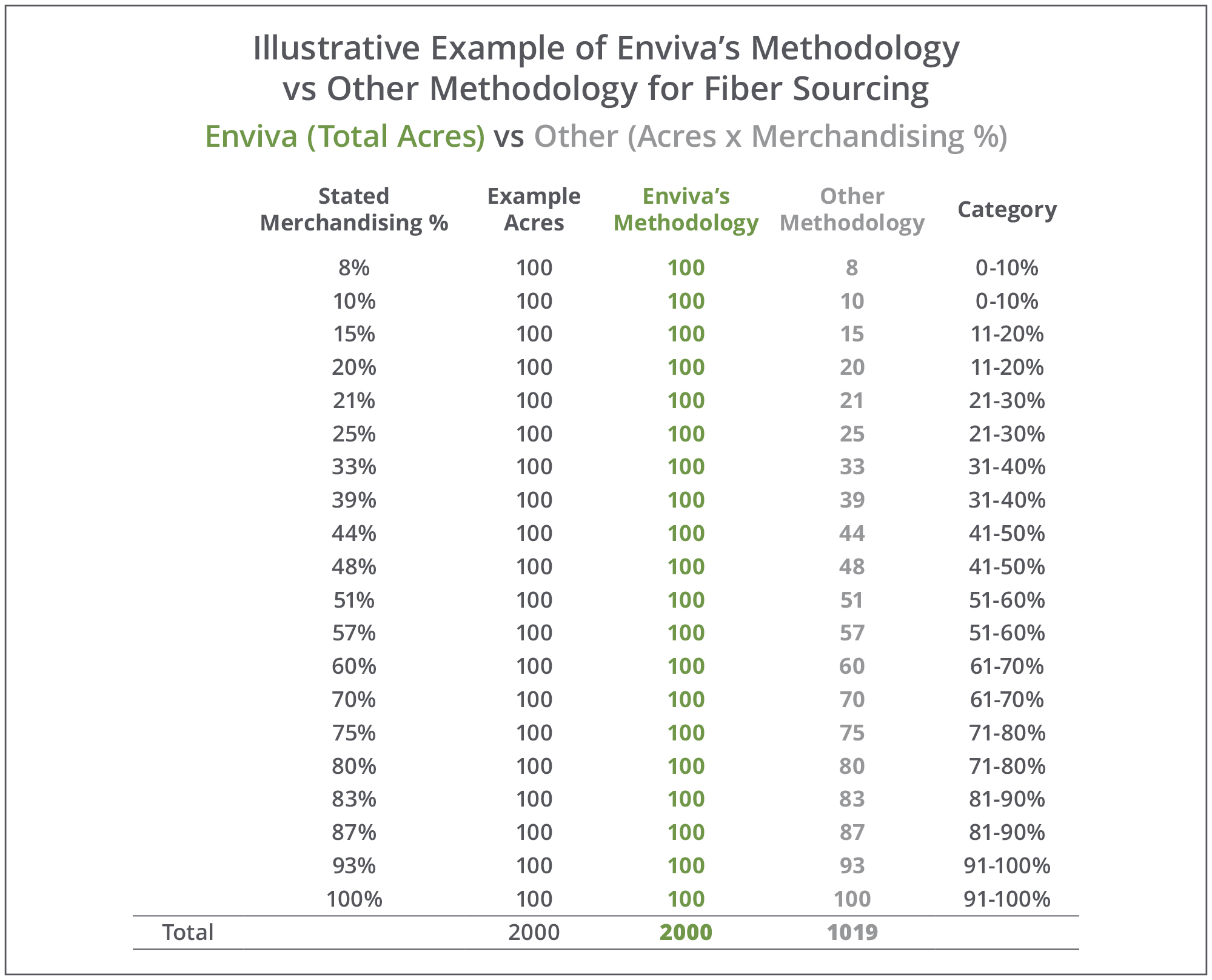

To illustrate, if one were to multiply the reported merchandising percentage by the number of acres in a harvest, one would draw incorrect conclusions about Enviva’s wood purchases. For instance, using the same example of a 100-acre harvest where we reported receiving 32% of the wood produced, such an approach would incorrectly suggest that Enviva procured from only 32 of the 100 acres, rather than procuring approximately 32% of the wood produced across the entire 100 acres harvested. Including only these acres in the merchandising percentage suggests that a landowner sells all of the timber to one customer, for instance Enviva, from a subset of the total acreage as opposed to the actual harvesting practices that generally produce a stream of multiple products for multiple customers across all acres and trees on the land.7 This approach would dramatically understate the harvested acreage from which Enviva was a small purchaser and similarly overstate the relative percentage of harvested acreage where Enviva is a larger part of the expected merchandising percentage.

Note the dramatically different conclusion which could result from an incorrect methodology applied to Enviva’s Track & Trace data.

-

High Percentage Merchandising Explained

Enviva’s sourcing also includes tracts located in regions where, due to land and soil conditions, it is difficult to grow sawtimber or where there are insufficient lumber markets. Given that the lower-grade material that is grown on these tracts is generally not suitable for high-value products, we and other purchasers of low-grade material can have a higher merchandising percentage of a tract. It is also important to note that, in certain circumstances, to support landowners seeking to improve forest health, Enviva or others will take a higher-than-average percentage of a harvest. This can be due to many reasons, including disease or storm damage, clearing to replant following previous, unsuccessful growth or forest management decisions, or when environmental and site conditions have led to unhealthy timber.

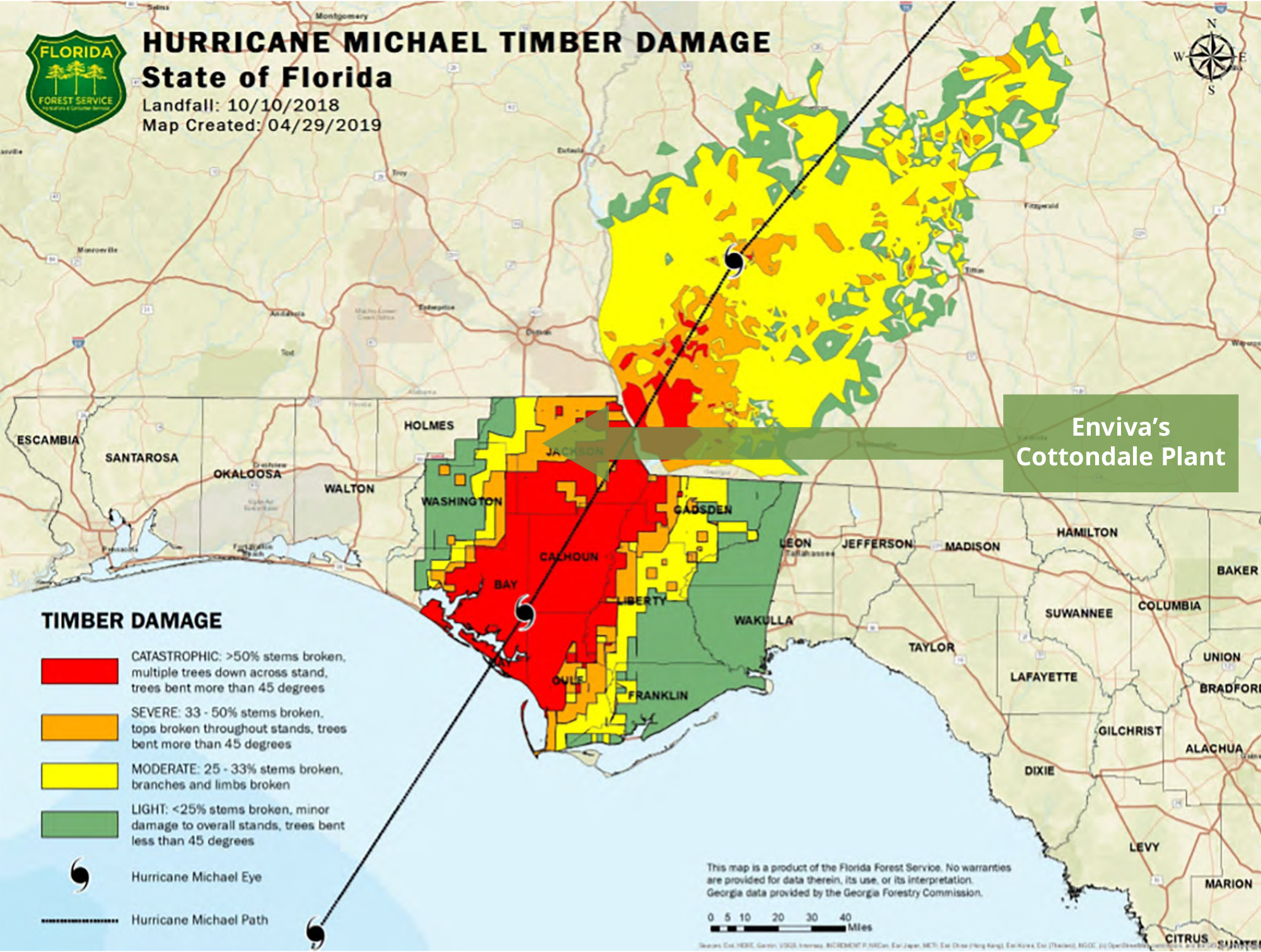

For instance, consider the sourcing region around our facility in Cottondale, Florida. In October of 2018, Hurricane Michael made landfall in northwest Florida with a massive, destructive impact on timber resources. Hurricanes and high wind events cause mature trees to snap, leaving damaged, jagged trees. The larger trees left on the ground quickly begin to decay and develop “blue stain,” a very undesirable condition in lumber, and the decay of the wood quickly affects the ability of the felled trees to be used in the pulp industry. Northwest Florida’s standing timber inventories were estimated to be reduced by 28% for pine and 19% for hardwood after the storm.

However, Enviva is able to utilize storm-felled wood, which allows the landowner to clear and then replant these damaged tracts, effectively resetting their land back to a productive, working-forest condition.

Similarly, these types of weather events also affect younger trees by pushing them into a leaning position by the strong winds. While the trees on the affected acreage may continue to grow, they are less useful for products like lumber or furniture. Consequently, at harvest, they will likely be merchandised to low-value purchasers like Enviva.

As the map below indicates, the catastrophic damage at the center of the storm’s path hit very close to Enviva’s Cottondale pellet production plant, and the company continues to source and report fiber from damaged tracts at higher-than-average merchandising percentages even four (4) years after the devastation.

Source: Florida Forest Service

Enviva’s Track & Trace data from the Cottondale sourcing region shows that the number of tracts with high merchandising greatly increased between 2018-2019, jumping more than 10-fold as landowners were finding ways to bring their forest lands back to working conditions.

Clearly, the U.S. Southeast forest landscape is complex and dynamic, and home to a robust forest products industry that provides multiple benefits to the economy, such as construction materials, personal care products, paper, boxes, utility poles, and bioenergy. Enviva is proud to be a small, but important, part of this vital community of forest stewards. This community’s collective decisions about planting trees for a range of products and markets have resulted in an increase in forest inventory in our sourcing area of 21% since 2011.

Resources:

1NCASI: Trends in Forest Harvest, Regeneration, and Management in the Southeastern United States as Related to Biomass Feedstock, Table 1. NCASI defines the Southeastern United States to include Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, North Carolina, South Carolina, Tennessee, Texas, and Virginia.

2FIA EVALIDator

The 3% harvested value represents the acreage of forest land that has been harvested in Alabama, Florida, Georgia, Mississippi, North Carolina, South Carolina, and Virginia compared to the total acreage of forested lands in these states in the USFS FIA database.

3NCASI: Forest Management Contributions to Biodiversity in the Southeastern United States; Biodiversity and Biomass Feedstock in the Southeastern US

4NCASI: Trends in Forest Harvest, Regeneration, and Management in the Southeastern United States as Related to Biomass Feedstock, Section 4.0. This value is calculated by dividing the annual growth by the annual harvest.

5The TimberMart-South data is based on purchases from Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, North Carolina, South Carolina, Tennessee, Texas, and Virginia.

6Merchandising percentage is not within the scope of our third-party verification audit of our Track & Trace process.

7We are confident in our methodology for maintaining privacy. Our Track & Trace program intentionally omits GPS coordinates and does not specify exact harvest locations to maintain landowner privacy. A disclaimer at the bottom of the T&T page speaks to this.

Preserving Supplier Confidentiality

To maintain the privacy of Enviva’s suppliers and landowners, tract points are located in the vicinity, but not the precise location, of the harvest. The tract GPS coordinates are fuzzed for security, and then altered again randomly to within 10 miles of their original location each time they are rendered in the map tool.